How Will London’s Driver Market Respond to Autonomous Vehicles?

Today's post comes from Tym Syrytczyk, co-founder of the Institute for Driverless Transport, an independent research organisation studying the implications and opportunities of autonomous transport in Britain. He also writes Self Driving Insights, a biweekly newsletter covering what driverless vehicles will actually mean for the country once they arrive.

After launching its robotaxi service in San Francisco, Waymo took just 20 months to become the city’s second largest ride-hail provider, overtaking Lyft to capture 27% of the market. Waymo plans to enter London by September of this year. Two further providers are targeting the same market: the British startup Wayve and China’s Apollo Go have announced that they will start robotaxi trials in the city this year. The prize of London’s market share is substantial. Estimates show that over 146 million taxi and private hire trips take place in London each year, the largest market in Europe.

Naturally, this has made the incumbent ‘human’ driver market, split between black cabs, and private hire drivers anxious over the future prospects of their jobs. So how will the London driver market respond to autonomous vehicles?

As you might imagine, many incumbent drivers will oppose autonomous vehicle rollouts. The average London driver works full-time at 45 hours a week. The skills that enable the jobs don’t carry as much value outside the cab and there is no adjacent career which can give drivers equivalent autonomy to what they already have.

Additionally, we know from recent history that black cabs are willing to mobilise against threats to their incomes. Uber entered London in 2012 and operated within a legal grey area. As Uber gained market share, thousands of cabbies took to the streets, blocking central London’s traffic on several occasions.

Yet, however disruptive Uber’s arrival was, it did not eliminate the need for drivers. It introduced a new class of competitor, but one that still relied on human labour. For black cab drivers, that meant there remained, at least in principle, an adjacent market they could enter by moving into private hire, even if that came with lower status, different working conditions, and the loss of the sunk costs invested in the trade. Robotaxis present a bigger threat, and so the politics of opposition will be sharper and broader than the backlash to Uber’s entry.

This piece gives the reader the tools to understand what opposition will likely emerge and lays out the dynamics that will shape this opposition. It will dig into the regulations that enabled robotaxi providers into London, the incentives at play for each player involved, and analyse the relationships between the technology providers, the incumbent drivers, and the regulators that have the power over the emergent robotaxi market.

What does London’s taxi market look like today?

London’s taxi market is complex. It includes the recognisable licensed black cabs, officially the ‘Hackney Carriage’ and ‘private hire vehicles’ which includes the newer app-based ‘ride-hail’ services provided by firms such as Uber and Lyft, as well as licensed minicab services that can only be accessed by pre-booking. From a consumer-facing angle the line between the services is blurring over time, for instance, black cabs can now be booked through the Uber app and on Freenow by Lyft. London has no cap on the total number of black cabs or private hire vehicles.

Nevertheless, the regulatory distinction between the different types of taxi services remains sharp. Black Cab drivers have a strictly regulated profession, one can only become a black cab driver if they pass ‘the Knowledge’ a test that started in 1865 and confirms that the future-driver has a near-perfect recollection of the thousands of central London’s streets. Typically test takers require 3-4 years to study for the exam. This, alongside the black-cab licensing fees and the purchase or rent of the Hackney Carriage vehicle represents a significant upfront cost. Whilst the qualification allows for flexible self-employment and a recognised license, it doesn’t provide much in terms of transferable career value.

As part of the tradeoff for these high regulatory costs, black cabs get to enjoy certain regulatory privileges. They can pick up passengers flagging them down on the street and get exclusive rights to taxi ranks. They also are exempt from the congestion charge, a £18 to £21 (USD equivalent) daily fee for driving in central London and can use bus lanes . While it is easier to become a private hire driver they don’t receive any of these privileges, with the exception of any electric vehicle drivers who are automatically exempt from the congestion charge.

The reasons why the next taxi conflict will not look like the last

The legal foundation for robotaxi entry is the Automated Vehicles Act 2024. The process to operationalise the Act known as ‘Secondary legislation’ set the basis for trialling and licensing driverless transport services, from robotaxis to autonomous buses (”automated passenger services”), as well as personal autonomous vehicle ownership.

The government’s intent became clear on 10 June 2025, when it announced that fully driverless transport licensing regulations would be brought forward to spring 2026, nearly two years ahead of the original end-2027 timeline. The broader regulatory package enabling scaled national deployment remains on course for the second half of 2027. Such accelerations are unusual: secondary legislation typically slips rather than advances, particularly under a new government. The move was the first clear signal that Whitehall intended to actively back autonomous vehicle deployment, and the first warning shot to incumbent drivers.

The multiple disrupting entrants problem

Several firms are now targeting London's robotaxi market: Wayve in partnership with Uber, Waymo, and Baidu's Apollo Go in partnership with Uber and Lyft. This complicates the incumbents' position. During Uber's entry, cabbies could focus their lawsuits on one or two targets. Now they face simultaneous entry from several players, each with its own public affairs operation lobbying regulators. When multiple firms independently advocate similar positions, regulators tend to read this as industry consensus, lending the disruptors a collective credibility that a single entrant could not achieve.

The sovereign AI problem

The Labour government has set its stakes, perhaps surprisingly, in favour of one of the robotaxi companies. When the government announced the licensing scheme, Wayve made its flagship announcement on the exact same day. This support ties into the government’s wider political ambitions to make the UK a leader in artificial intelligence deployment, ambitions they consider Wayve central to.

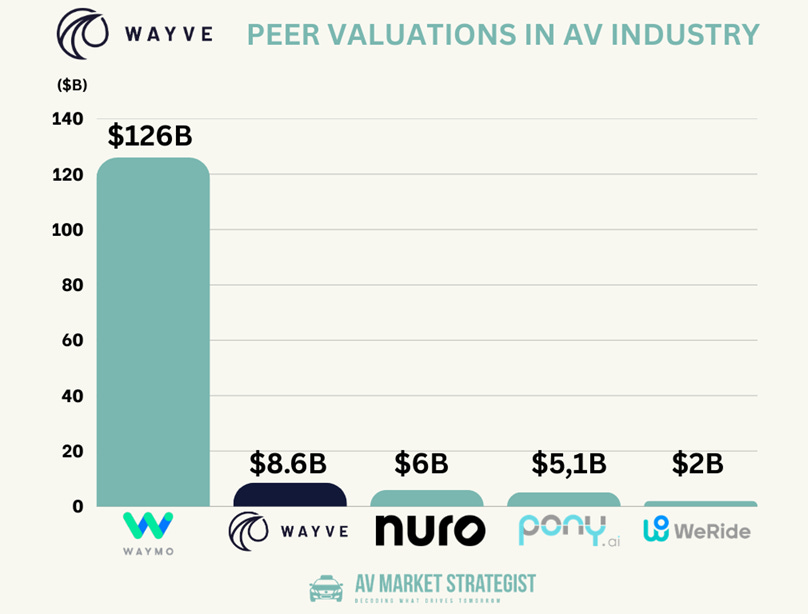

The UK government’s enthusiasm for AI sovereignty means that policymakers are considering the success of domestic AI firms as favourable to British national interests. The government is closely collaborating with Wayve. Three Cabinet members celebrated the firm’s Series D raise of $1.5bn at an $8.6bn valuation, and the government’s flagship £500 million Sovereign AI venture fund will be launched at a Wayve-hosted event. As Wayve’s London deployment is its first global commercial release, it will be competing directly against the larger, better-funded Waymo. Any intervention slowing the London robotaxi market would disproportionately harm Wayve, making such measures deeply unattractive to the current government.

When can we expect opposition?

Opposition will mobilise quickly. The CEO of Addison Lee (no paywall), a major private hire provider which holds partnerships with black cab drivers, has already called for “minimum pricing” on robotaxis citing the risk that better-funded tech firms will undercut human-driven services and jobs. The incentive to act early is clear: regulations are easier to shape before a service is established, and public scepticism of robotaxis will be highest before deployment. San Francisco data suggests this window is short, with net favourability towards autonomous vehicles rising 45 points within two years of deployment.

Novelty attracts media attention, and incumbent drivers will not want early coverage to be one-sided. Every major autonomous vehicle announcement has already drawn pushback from incumbent drivers in press coverage, and both sides know that public approval drives customers and gives policymakers cover to act in their favour.

Will the incumbents (Black cabs and ride hail drivers) coordinate between each other?

Black cabs are well-positioned to coordinate opposition across multiple channels. Their membership spans many national and industry-specific unions, and the Licensed Taxi Drivers’ Association alone represents over 10,000 of London’s 16,000 licensed black-cab drivers. Local authorities routinely treat taxi drivers as a key stakeholder group, consulting them on transport and road changes. Ride-hail drivers, by contrast, face greater coordination challenges, unionisation rates among app-based drivers are likely low, and Uber drivers’ past protests failed to disrupt service access.

As for coordination between black cabs and private hire drivers, no institution bridges the two sides. The closest attempt came from the GMB union, which in the early 2010s represented both black cab and private hire drivers, until Uber’s arrival made this untenable. The GMB’s anti-Uber stance clashed directly with its Uber driver members’ interests, and those drivers eventually broke away to form their own organisations.

Who will the opposition target? What methods will they use? And what may they demand?

Incumbent drivers can lobby a range of bodies to protect their interests: national government, Transport for London, local authorities, and on the private side, firms such as airports and train stations that operate taxi pick-up zones.

Black cab drivers have historically deployed every available method: lawsuits, protests, media campaigns and lobbying at national and local government consultations. A 2014 lawsuit against Uber over the legal definition of a taxi meter was one such battleground. Backed by established union infrastructure, they will bring these same techniques to bear against robotaxi entry.

Incumbent drivers’ demands will vary by audience. At the national level, they will push for regulations that raise the price and inconvenience of robotaxi services to keep their own offerings competitive. Addison Lee’s call for minimum robotaxi pricing is an early example. Opponents will test different arguments, gravitating toward whatever best mobilises public opinion.

Arguments likely to land with the public include a call for greater accessibility requirements: all black cabs must be wheelchair accessible by law, yet no London robotaxi trial has modified vehicles beyond a standard car. Incumbents drivers could demand equivalent requirements, raising costs for operators. Further options include mandatory insurance levies and legal challenges to TfL licensing grounds that secondary legislation was rushed. Central government’s endorsement of the technology will, however, make persuading policymakers difficult.

At the local level. Planning permission for robotaxi charging and cleaning depots are likely to become a key target: in the UK, most developments, even on private land, require community consultation. At these planning committee hearings, members of the public can sway councillors to block or modify proposals on grounds such as noise, traffic, or aesthetics giving organised opposition a ready-made lever to reduce the on-the-ground infrastructural capacity of their competition.

Conclusion

The arrival of autonomous vehicles in London will be contested, litigated, and protested in the streets, the planning committees, and the corridors of Westminster. But the politics of this disruption are structurally different from the last. Incumbent drivers face legally entrenched opponents, multiple simultaneous entrants, and a central government that has, at least in the case of Wayve, bound the prestige of its technology policy to the success of the firm.

Their strategic window is narrow. The goal will be to secure durable regulatory constraints before public opinion and political momentum shift decisively against them. San Francisco offers a cautionary precedent: even Cruise’s collapse and the subsequent public backlash against autonomous vehicles did not prompt ride-hail drivers to mobilise against Waymo. London’s incumbents will be watching the new firms’ approval ratings closely. They will need to move quickly, and together, if they are to shape the market that emerges.

- Tym

| A guest post by

|