New Data Shows AVs Starting to Bite Into Human Rideshare

Autonomous vehicles are starting to impact rideshare markets. Gridwise data shows fewer trips per hour for drivers in AV cities.

We covered Gridwise Analytics’ previous Autonomous Vehicle Impact Report when it was released in 2025, and the company has now published its 2026 update. The new data provides one of the clearest early looks yet at how robotaxi deployments are continuing to affect traditional rideshare markets.

The changes are still relatively small, but the data suggests that in a few AV active cities, autonomous supply may be beginning to show up in the broader ride hailing ecosystem.

AVs Are Not Just Coming – They’re Already Here

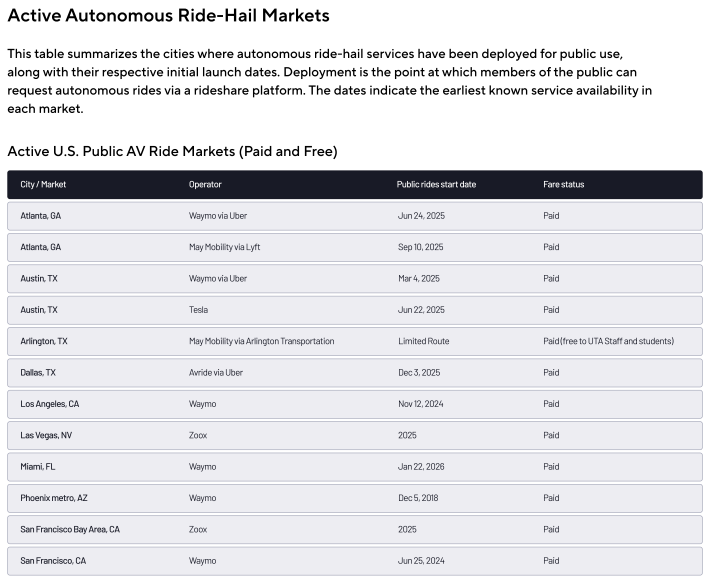

AVs are operating commercially today in cities like Atlanta, Austin, Los Angeles, Phoenix, and San Francisco. These markets provide early indicators of how autonomous services from pilot programs to limited public robotaxi services interact with existing rideshare ecosystems.

Gridwise’s report analyzes proprietary driver data from Q1 2024 through Q4 2025, comparing AV-active markets to nationwide trends in driver productivity and earnings.

The big question: Are autonomous vehicles actually impacting human rideshare drivers yet? The short answer from the data is yes, but the full story is nuanced.

Trips per Hour Are Falling Faster in AV Cities

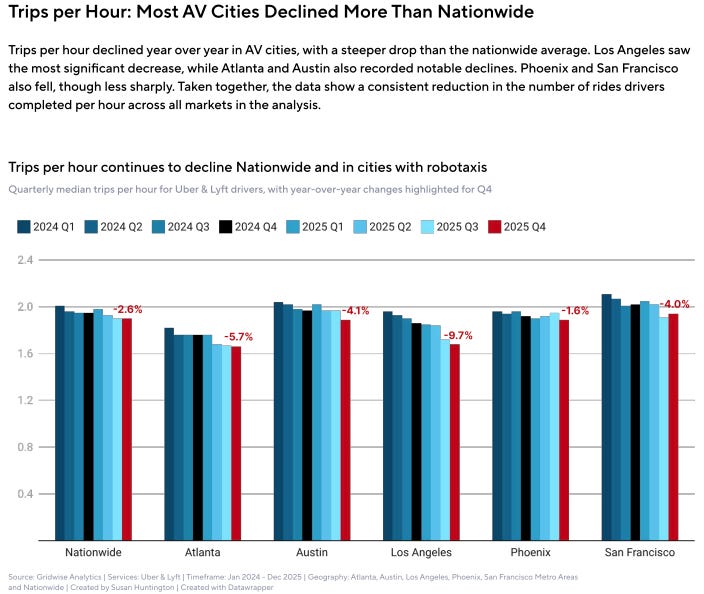

One of the clearest signals emerging from the report is that human rideshare drivers in markets with active AV deployments are experiencing steeper declines in trips per hour than the rest of the country.

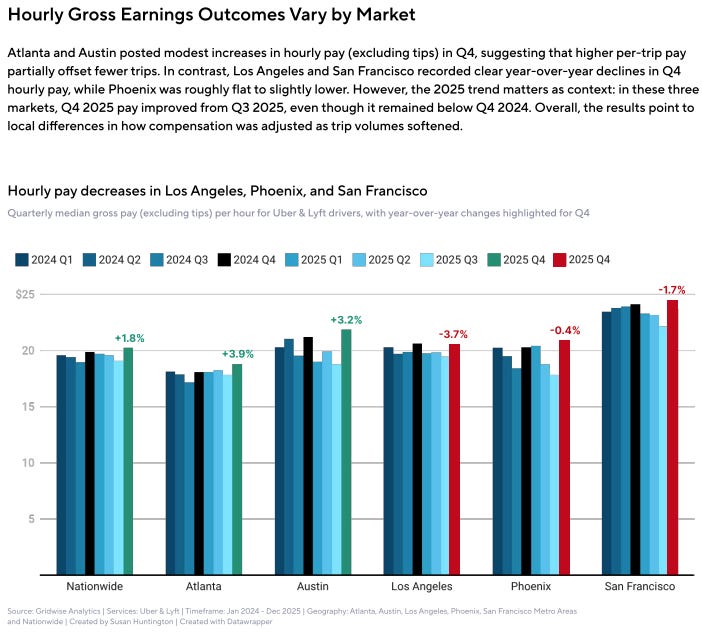

Gridwise found that in Q4 2025, trips per hour fell by approximately 5.3% in AV markets, compared with a 2.6% decline nationwide. In Los Angeles, the decline was especially pronounced, nearing a 10% year-over-year drop.

This metric is important because trips per hour are a proxy for driver productivity, essentially how much work a driver can accomplish in a given shift. A larger drop suggests that demand is being siphoned off, either by reduced trip volumes or increased competition for the remaining rides.

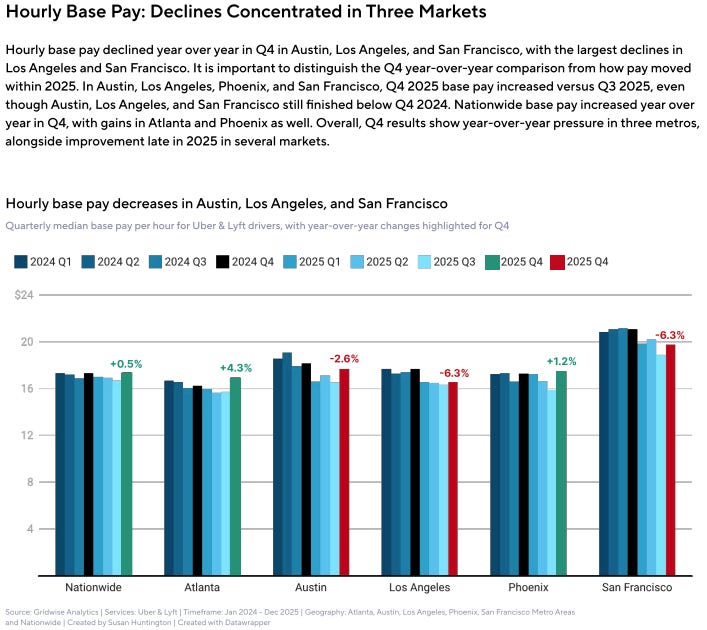

Earnings Are Taking a Hit in Some Cities

The productivity declines seen in AV-active markets are also showing up in driver earnings. While the national average hourly gross pay for drivers increased slightly (around +1.8%), several AV markets saw year-over-year earnings declines. Los Angeles experienced about a 3.7% drop, San Francisco saw a 1.7% decrease, and Phoenix reported a small 0.4% decline.

The link between productivity and earnings isn’t surprising: fewer trips per hour, all else equal, usually means fewer dollars in the driver’s pocket. That’s the concern for traditional drivers in markets where autonomous services are filtering into demand pools.

Not All Markets Are Equal

It would be easy to read these early trends as a uniform decline for all human drivers in AV cities, but the report and related analyses suggest a more complex picture. Some AV cities show mixed results for driver utilization: the share of time drivers spend with passengers versus waiting for rides.

In Austin and Phoenix, for example, utilization has shown modest gains despite broader trends.

This underscores an important point: AV impacts aren’t monolithic or evenly distributed.

Variables like local population trends, rideshare demand patterns, tourism cycles, and platform strategy can all tilt outcomes differently from city to city.

Why AVs Affect Rideshare Drivers

So what’s driving these shifts? There are several intertwined factors:

Increased Supply via Robots: Autonomous fleets add supply to the platform ecosystems that were once exclusively human-driven. Even if AV miles are still a small fraction of total rideshare miles, their presence is diluting demand for human drivers in specific areas.

Price Competition Pressure: According to projections cited in the Gridwise report, AV profitability at scale likely requires pricing near $1 per mile, significantly lower than average human rideshare fares, which hover closer to $3.25 per mile. That pricing dynamic could create downward pressure on prices and force platforms to push AV services into price-sensitive segments first.

Shifts in Platform Strategy: Rideshare platforms are constantly optimizing algorithms for supply, demand, and pricing. The presence of AVs adds a new data layer that can affect how these algorithms prioritize ride assignments, surge pricing, and driver incentives in certain geofenced areas.

How Fast Will AVs Overtake Human Drivers?

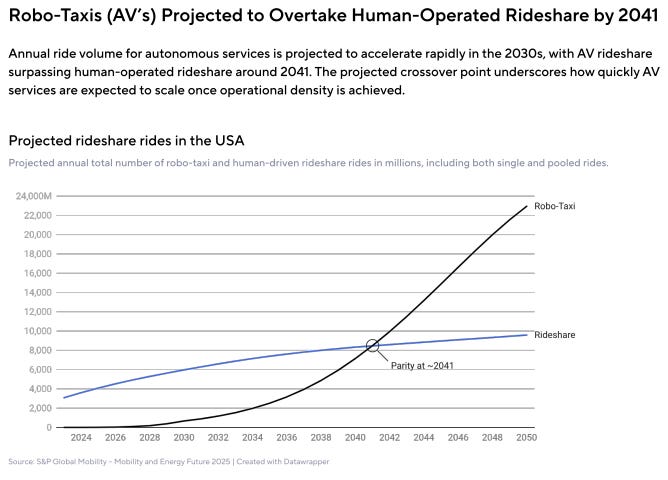

Despite early impacts, AV vehicles are not poised to replace human rideshare drivers tomorrow. According to S&P Global projections referenced in the report, autonomous services aren’t expected to achieve parity with human-driven rideshare markets until around 2040–2041, a timeline measured in decades, not years.

This suggests that while AVs are affecting micro-dynamics in select markets today, human drivers will remain central to rideshare services for a long time. Drivers and platforms alike should expect gradual shifts, not overnight displacement.

What This Means for Drivers

For drivers in AV-active cities, the message isn’t alarmist, but it’s a wake-up call. Here’s what matters most:

Monitor local earnings and productivity trends: Market conditions can diverge dramatically from national averages.

Watch pricing and incentive changes: Adjustments in platform economics may signal broader strategic shifts related to AV deployment.

Stay adaptable: As AV technology and platform strategies evolve, readiness to shift focus across markets could make a difference in earnings resilience.

The Gridwise report presents early evidence that autonomous tech is beginning to have real economic impacts on human rideshare drivers, but it also shows that human drivers are far from obsolete. The future of rideshare will likely be a hybrid ecosystem with humans and robots serving different segments, prices, and contexts for many years to come.

Understanding these market forces now can give drivers a strategic edge as the autonomous era continues to unfold.

My Take

The Gridwise data confirms what many industry observers have been watching in cities like Los Angeles and San Francisco: robotaxis are starting to show up in the data.

Autonomous vehicles are not replacing human drivers overnight, but they do appear to be nibbling at the edges of rideshare demand in a few early markets. A 5 to 10% drop in trips per hour might not seem huge, but it is one of the first quantitative signals that AV supply may be starting to affect the broader ride-hailing ecosystem.

At the same time, the sky is not falling. Most projections still suggest that large scale displacement of human drivers is likely decades away. What we are seeing now looks more like the early stages of a hybrid phase, where robotaxis handle simpler, highly repeatable trips in dense urban areas while human drivers continue covering everything else.

For the AV industry, the takeaway is that the transition may be slow but it is becoming measurable. The more robotaxi fleets expand in cities like Phoenix, San Francisco, Los Angeles, and Austin, the easier it will be to see how AV supply changes the dynamics of the broader ride-hailing market.

- Sergio

| A guest post by

|

This is all really interesting but I think the bet on the speed of the switch to AV from S&P is super conservative. I think we're all going to be blown away by how fast the flywheel moves once it gets going.

Harry, thanks I enjoyed your summary and analysis.

Echoing what Brady said, it seems like the transition could happen much faster than you lay out.

The analysis you highlighted concluded that AVs were having a small but noticeable impact on rideshare economics in 2025. That's during a period when the total number of commercial AVs went from ~2,000 to ~3,000.

Looking forward, Waymo is potentially going to put 50,000+ AVs on the road over the next 3 years. Here's one of several partnership they are pursuing:

https://finance.yahoo.com/news/waymo-mulls-2-5-billion-003105155.html

50,000 / 3,000 = 17x. A 17x scale up over 2025 numbers should have a much larger impact on rideshare than we saw in 2025. And that's just Waymo - Zoox, Tesla, AVride, Nuro/Uber/NVIDIA/Lucid, and more are all going to be putting thousands of AVs on the road as well.

I agree that exurban and rural areas will be much slower to feel these changes than urban and 1st ring suburbs.

In 2030, for major metro areas from New York down to ~St. Louis in size, don't you think the rideshare market looks very different from today?

I appreciate your insight here.